Initial Coverage - MARK.JK | 07 December 2021

MARK Dynamics Initiation Report - Indonesia’s best play for Omicron Concern

BUY TP: IDR1,600

For Full Report, Download Here:

https://bit.ly/MarkInitiation

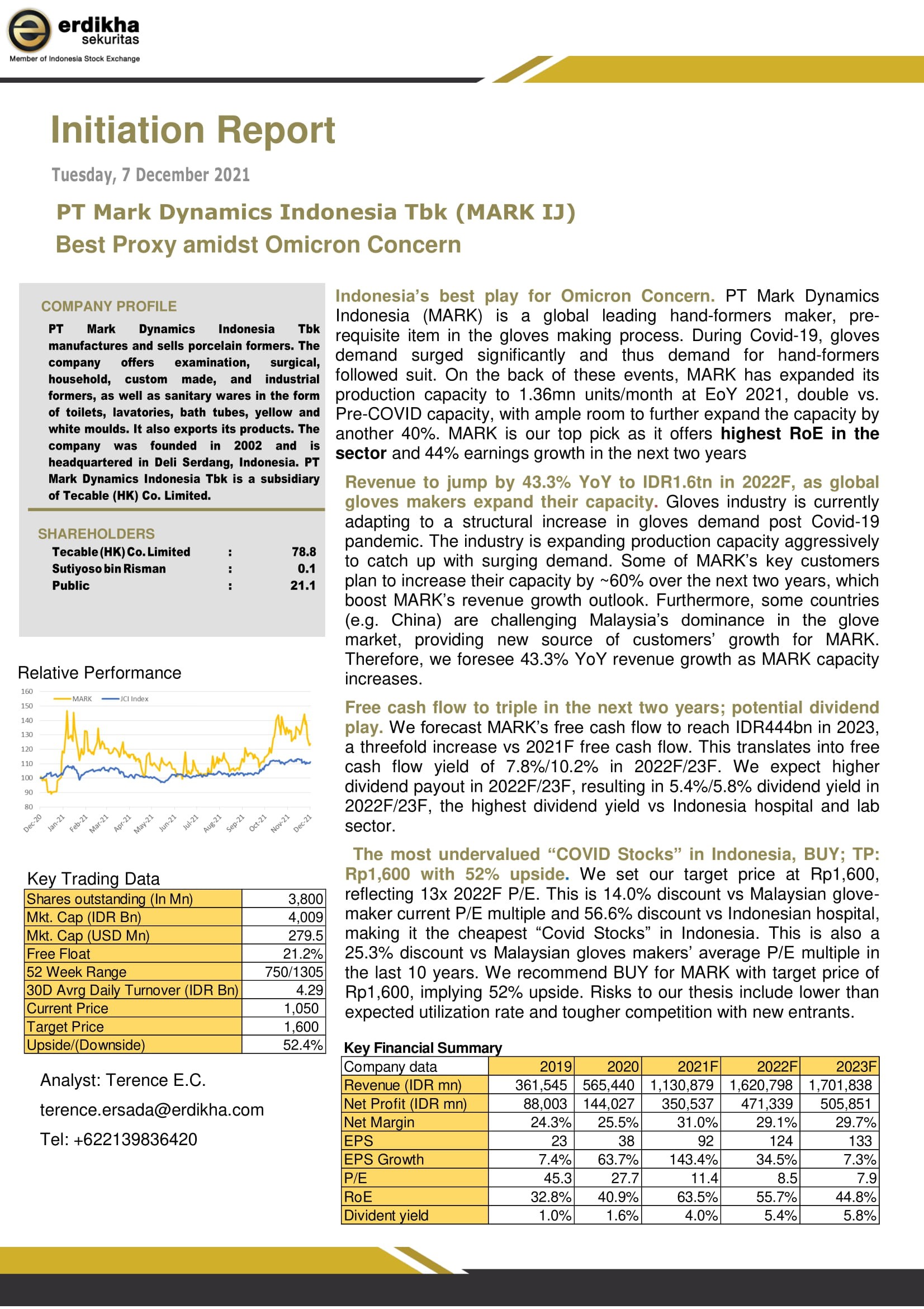

PT Mark Dynamics Indonesia (MARK) is a global leading hand-formers maker, pre-requisite item in the gloves making process. During Covid-19, gloves demand surged significantly and thus demand for hand-formers followed suit. On the back of these events, MARK has expanded its production capacity to 1.36mn units/month at EoY 2021, double vs. Pre-COVID capacity, with ample room to further expand the capacity by another 40%. MARK is our top pick as it offers highest RoE in the sector and 44% earnings growth in the next two years.

Revenue to jump by 43.3% YoY to IDR1.6tn in 2022F, as global gloves makers expands their capacity.

Gloves industry is currently adapting to a structural increase in gloves demand post Covid-19 pandemic. The industry is expanding production capacity aggressively to catch up with surging demand. Some of MARK’s key customers plan to increase their capacity by ~60% over the next two years, which boost MARK’s revenue growth outlook. Furthermore, some countries (e.g. China) are challenging Malaysia’s dominance in the glove market, providing new source of customers’ growth for MARK. Therefore, we foresee 43.3% YoY revenue growth as MARK capacity increases.

Free cash flow to triple in the next two years; potential dividend play.

We forecast MARK’s free cash flow to reach IDR444bn in 2023, a threefold increase vs 2021F free cash flow. This translates into free cash flow yield of 7.8%/10.2% in 2022F/23F. We expect higher dividend payout in 2022F/23F, resulting in 5.4%/5.8% dividend yield in 2022F/23F, the highest dividend yield vs Indonesia hospital and lab sector.

The most undervalued “COVID Stocks” in Indonesia, BUY; TP: Rp1,600 with 52% upside.

We set our target price at Rp1,600, reflecting 13x 2022F P/E. This is 14.0% discount vs Malaysian glove-maker current P/E multiple and 56.6% discount vs Indonesian hospital, making it the cheapest “Covid Stocks” in Indonesia. This is also a 25.3% discount vs Malaysian gloves makers’ average P/E multiple in the last 10 years. We recommend BUY for MARK with target price of Rp1,600, implying 52% upside. Risks to our thesis include lower than expected utilization rate and tougher competition with new entrants.

{kind=link}